Omid Malekan

哥伦比亚商学院加密教授、作家,加密监管与市场知名评论员

Twitter

观点

Noah makes very good points in this article, but I disagree with his defense of chargebacks given how they are structured today.

The thing everyone forgets is that while payment systems that allow chargebacks (like credit cards) protect consumers, they do the opposite to merchants.

The data on this varies, but something like 40 to 60 percent of all credit chargebacks are "friendly fraud", AKA people abusing the feature for something it wasn't meant for.

In what other context do we defend a solution this ripe with abuse? But cards perpetuate themselves due to a complicated mix of sticky behavior and anti-competitive collusion.

If people want insurance for their transactions (which I certainly do) they should just pay for it, like any other insurance. They would file claims much more judiciously if they did. It also doesn't make sense to make your local Deli pay for your loyalty to American Airlines.

Stablecoins are an opportunity to revisit this strange setup, first and foremost by elevating new payment systems that a corporation does not control (unless the network is permissioned).

Certainly if agents start useing stables, as Noah argues, that will open the door for their owners to start to too.

The other wildcard in this debate is whether the US government caps swipe fees like many other countries have. Now that we know Wall Street hates competition and is more than willing to use regulations to harm consumers, it would only be fair.

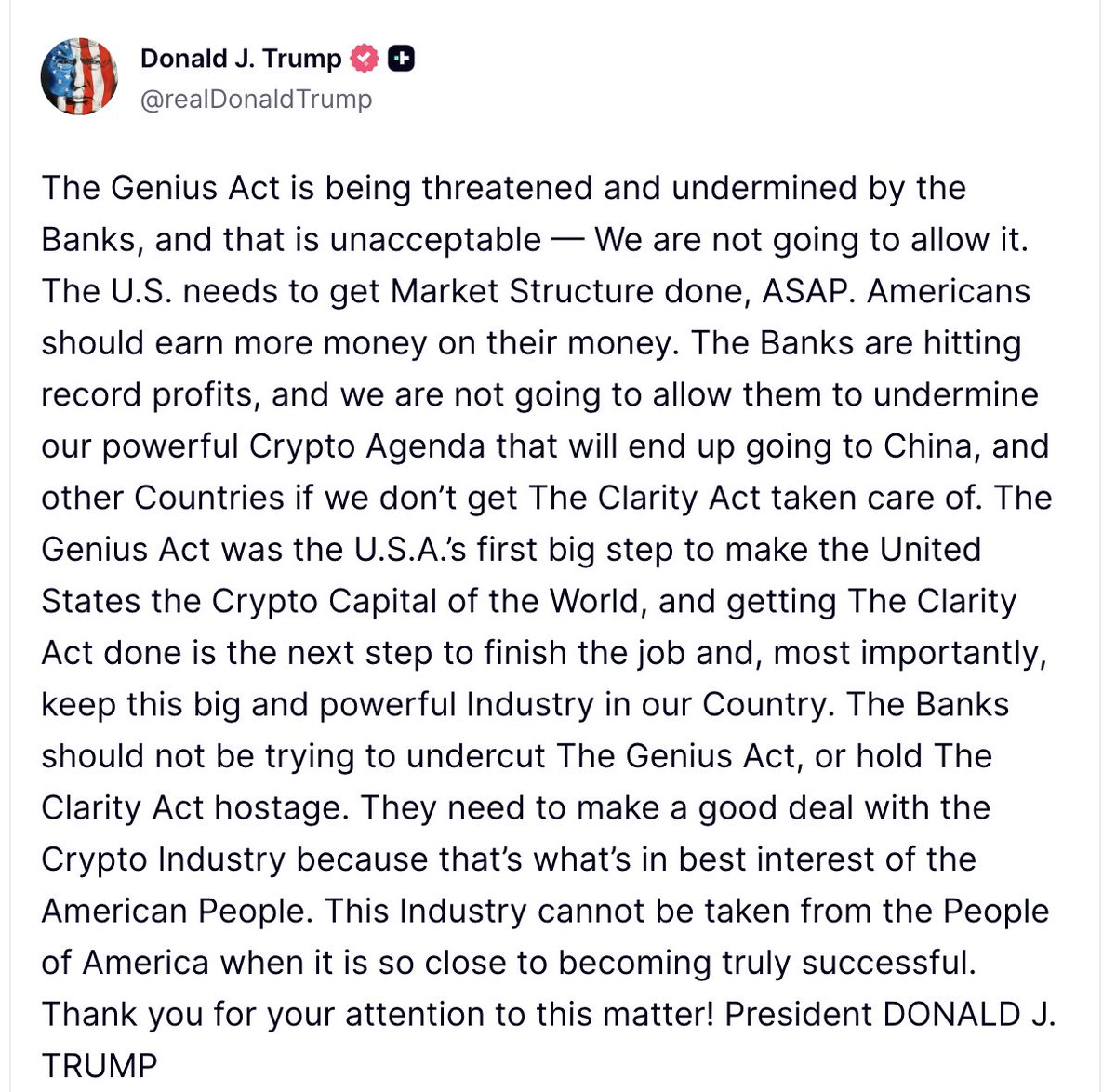

Glad to see that the President lands on the side of logic and sanity on the stablecoin yield issue. Banks make plenty of money. American savers deserve options. Competition is good. If selfish anti-American Wall Street lobbying kills crypto progress then foreign jurisdictions prevail.

Vitalik's new approach to L2s is how many of us understood them in the first place: Rollups expand the expressibility and customizability of Ethereum security.

Some optimize for a different tech stack. Others for usability, and yet others for scale. L2s let devs and users choose their own adventure.

This is what I meant when I said that the monolithic chain approach is cryptoeconomic socialism and the modular capitalism.

All of TradFi is modular in some way, because it makes practical and economic sense to offer a spectrum. The crypto version is superior however, because it's the devs and users who decide which part of the stack they use, not the Suits or the Man.